Contour’s consultant in Turkey, Meral Sengoz, shares her insights on why the digitalisation of international trade has not reached critical mass and what factors are needed for banks, corporates and the logistics industry, to embrace paperless trade. Here is an excerpt of the original blog.

The digitalisation of international trade is among the most studied topics, especially after the Covid-19 Pandemic.

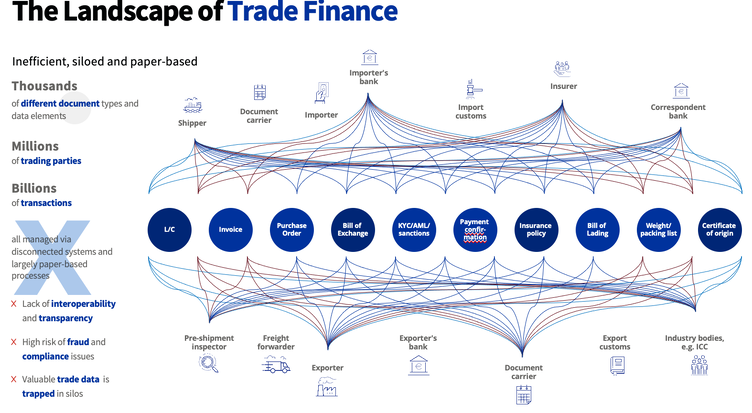

With the advent of Artificial Intelligence, namely chatGPT and with the launch of Apple’s mixed reality glasses, the world’s first wearable computer called “Vision Pro”, it is hard to believe that more than USD 25 trillion [1] of international trade is still done on paper.

Undoubtedly, Distributed Ledger Technology (DLT) or blockchain is the most important technological breakthrough enabling the digitalisation of international trade.

In international trade, however, it seems that the excitement generated by DLT is not spreading as quickly as expected.

Why can’t digitalisation be achieved in international trade? What are the root causes of the delay?

The diversity of the parties in international trade, the differences in legislation between countries, the very traditional structure of international companies, especially in the maritime industry, and the lack of trust in new and disruptive technologies in the protection of the sector’s precious “commercial data” are the main challenges for the “digital leap” in this sector. On top of that, when use cases vary according to their different sectors and trade regions, it becomes tough and takes time to establish “standards”, which are indispensable elements in the use and transfer of electronic trade data.

In fact, the maritime industry’s EDI (Electronic data interchange) dating back to the 1970s is still used, and today’s technology that provides easy and real -time data sharing is preferred to API. It’s hard not to wonder why EDI, which is almost as old as the discovery of Container and the number of experts who know the software codes, is still preferred. I think the answer is the addiction to tradition and habit that is a part of all of our lives!

Although it is extremely cumbersome and inefficient, there is a functioning order among the parties of international trade. Archaic technological structures and manual workflows are intricately intertwined, and the courage to renew these structures with new cutting-edge technologies, especially DLT, emerges in relatively few banks, logistics companies, fintechs and countries. In addition, due to the absence of legal regulation and the lack of auditing institutions, a vicious cycle occurs that inhibits the adoption of trade digitalisation.

As a result, my experience in banking and fintech, including European banks and companies, has shown that the phrase, “There’s no need for invention now” is not just a phrase unique to Turkey.

On the other hand, Asia-Pacific banks and corporates are not afraid to invest in DLT and other disruptive technologies, and unlike Europe, they do not hesitate to enrich their experiences. For example, in countries such as China, India, Singapore, and Malaysia, which heavily use letter-of-credit payments, the interest in Contour Network [2], which is one of the best examples of DLT and uses Corda technology, is quite high.

When will the logistics industry voluntarily embrace paperless trade and the use of DLT?

80% of [3]the trade volume in the world is carried by the maritime sector. Although there have been various initiatives in digitalization of shipping sector such as Tradelens in the past [4], it is not difficult to predict that this complex and cumbersome industry will lag behind other trade parties. In fact, there are no developments that would be a threat to this conservative stance!

As soon as the eFTI [5]((Electronic Freight Transport Information) is implemented in the European Union in 2024 and the “Electronic Trade Documents Bill” of the UK, is enacted, the legal basis will be set, and the move to abandon paper-based traditions in the transport sector, including maritime, will accelerate. International and regional agreements by governments around the world will further accelerate this migration.

The Port Authority, which provides physical and technological infrastructure services to the logistics sector, or the Logistics Hubs, which provide multi-transportation, are the areas that I pay the most attention to. After all, ports are where goods are loaded onto ships and delivered to buyers at their destinations.

Online and real-time communication between ships, freight forwarders, importer and exporter companies with port authorities is essential for goods to be completed and delivered to buyers. However, ports are heavily dependent on the logistics sector; so, again, complex commercial relations, outdated structures and dependencies that are intertwined appear as a problem here as well.

Let’s come to the insurance sector, which is a sector that is sticking to its outdated habits as the logistics sector. While they expect the logistics industry to digitalise, they will continue to keep their silence until the logistics industry and banking sector goes digital.

Are banks progressing in implementing DLT and digitizing trade finance?

Banks have invested a lot in digitalisation, especially after the 2008 crisis. Banks that have legal obligations and are subject to sanctions with high penalties for non-compliance, have seriously taken the lead in digitalisation activities to make their operations efficient due to OFAC, KYC rules.

Moreover, they have not hesitated to integrate with Open Banking and Fintech institutions, taking API and Cloud technology with them. Banks have learned to create technology-based collaborations in a very short time.

In my opinion, the closest parties to the vision of digitalisation in international trade and finance are the banks and financial institutions.

However, banks face difficulties establishing DLT-based cooperation with importers, exporters and their correspondent banks. Due to the issues listed below, they appear reluctant to adopt disruptive technology in this field:

- Banks continue to feel dependent on the cumbersome service offered by SWIFT as they have not established joining new digital networks in the Letter of Credit (LC) product that combines the movement of physical goods, money and the payments of those goods. It takes 15-20 days to complete a LC transaction with traditional methods. This situation and prolonged reserve processes not only hinders the cashflow of corporates, but also causes high operational costs due to the goods waiting at the ports for appropriate document delivery. SWIFT’s insufficient and completely manual letter of credit flows play an important role in the lack of financing needs of corporates with a value of USD 1.8 trillion in the world. What a waste of time, energy and money, isn’t it?

- Bills of lading or transportation documents, which prove that the goods have been loaded, are one of the most basic documents that enable banks to make payments under LC transactions. However, these documents are still moved between banks in paper form by courier companies such as DHL. Due to the late arrival of these papers, the “letter of indemnity” (LOI) practice has become a compulsory requirement. In other words, with the approval of the banks, the goods are delivered to the importer by the carrier without existence of a paper bill of lading. This practice not only puts banks in a difficult spot, but also causes companies to deposit collateral with banks for LOI and incur extra costs. Most of the time, this process causes friction between the bank and the importers. SMEs do not have the advantage of large corporates that can solve their problems by establishing a trusted relationship with banks.

As a result, although banks want to adopt technology to digitalise, they still find themselves dependent on paper-based traditions of the logistics sector and are stuck in a chicken-and-egg dilemma.

Is collaboration with fintechs a risk or an opportunity? Even if there are some risks, why should we go through this experience?

Bankers don’t like to take risks, but banking is about managing risk and making money.

Here is my analysis from the point of view of a former trade finance product manager of a leading bank that has conducted the first DLT transaction in Turkey, and has had the opportunity to work with international fintechs:

- DLT is already the technology of today, not the future. While its use is not widespread; that’s not a problem because we will be enriched by a great mindset change from the workforce and top management who need to be prepared for digitalisation.

- SWIFT’s LC messages are known and accepted by every banking player, and we have designed our infrastructure accordingly. But it is not difficult to integrate back offices with new technology. In addition, by shortening the LC process, we can gradually shift staff from operations to technology and integration, rather than making immediate changes to the existing infrastructure.

- It can be difficult to get out of the comfort zone to bear the cost of persuasion and training of in-house teams. It is essential to be efficient and to bear these costs in order to be prepared for the future and for survival.

- There are significant concerns in explaining these new technologies and formations to the profit or return-oriented senior management. Focusing on the medium and long term rather than short-term results and returns is the only way forward.

- Let other institutions try it out first. However, if you are late to learn the new technology, more costs will be incurred in the future, adoption may be delayed due to the lack of trained workforce and the competition may be delayed.

- The digitalisation of the logistics sector is a priority, but don’t wait for it to happen first. Digitisation has many dimensions, from data standards to digital legal entity identity. When AI combines with IoT, Blockchain (DLT), 5G, the picture will grow and we have to start learning from somewhere.

- Transaction processes are shortened and efficient on the DLT based platform, but there are not enough banks and companies in the network yet. As soon as you realize that a platform or technology can do your job, you have to start somewhere. If there is a good solution, other trading partners will definitely join in time.

- It may be difficult to explain new technologies to corporates. Onboarding to new platforms can be challenging, but processes are not as difficult as they used to be.

- It is necessary to examine complex private law agreements for membership to platforms. However, fintechs who are aware of this have simplified their legal documents considerably in the last few years. In addition, trade-based electronic records will be legally accepted as a result of a recent major change in English law, which is the legal basis for most international trade agreements. In this case, the use of rulebooks on digital platforms will become less relevant.

In conclusion

The use of the new disruptive technologies in the field of international trade is unavoidable. In order not to lose their competitive edge, banks and companies must closely follow and understand all the digitalisation studies, the products, digital solutions and new cooperation networks offered by fintechs. They must bear the learning costs and be bold in gaining experience.

This article has been extracted from the full post here. To learn more about trade digitalisation in Turkey, follow Meral on LinkedIn. Contact us now to embark on your digital trade journey.